Drawing on industry reports, financial analyses, and geopolitical assessments, this report synthesises the strategic priorities for mining executives in 2025.

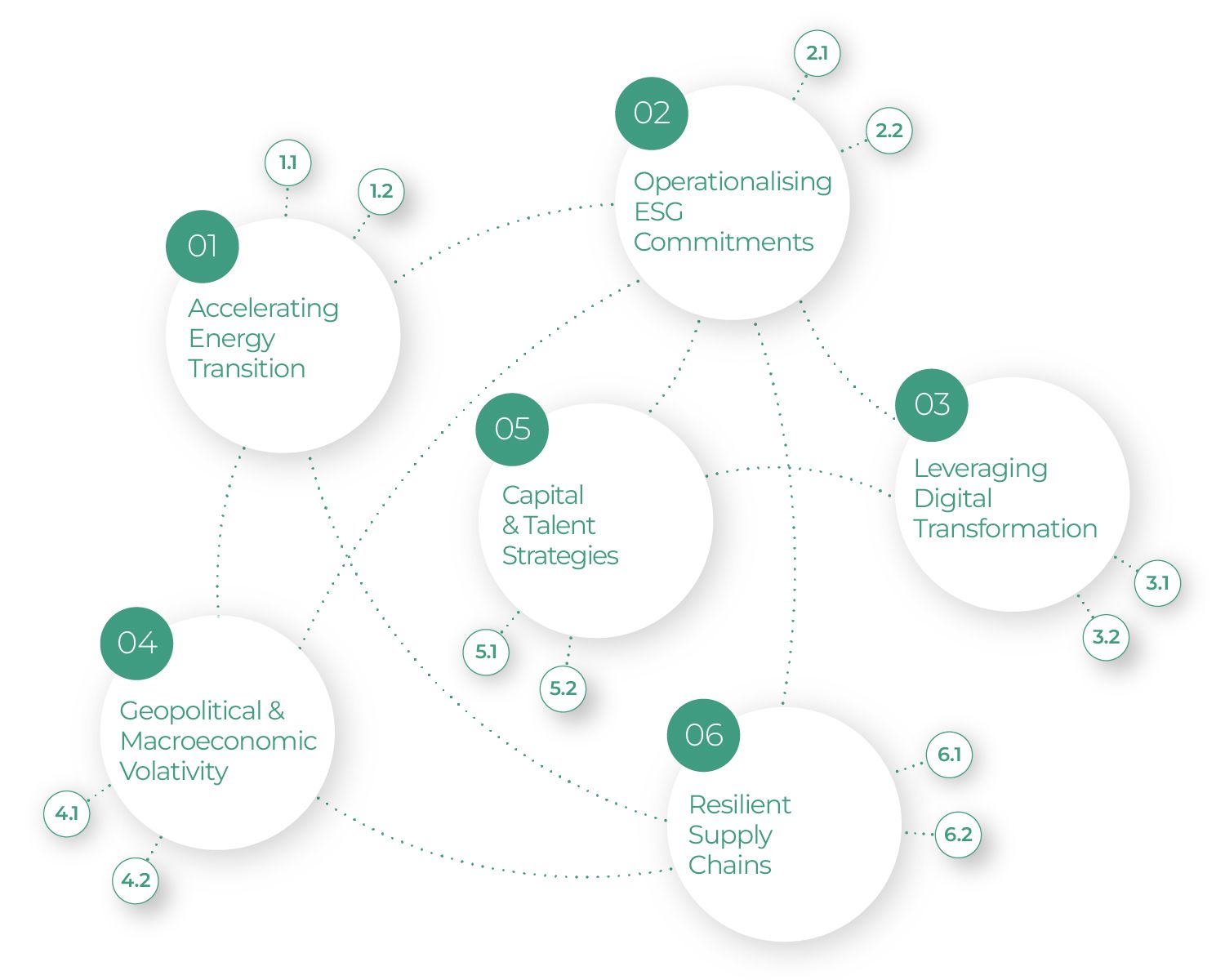

1. Accelerating the Energy Transition Through Critical Minerals

The decarbonisation of global economies remains the dominant demand driver for mining companies. With renewable energy infrastructure, electric vehicles (EVs), and AI-driven technologies requiring unprecedented volumes of copper, lithium, cobalt, nickel, and rare earth elements, CEOs are prioritising investments in projects aligned with these commodities. The International Energy Agency (IEA) estimates that global critical mineral demand will quadruple by 2040 under net-zero scenarios, yet current supply trajectories fall short, creating structural deficits[1][8].

1.1 Securing Supply Chain Dominance

Strategic consolidation through merger and acquisition (M&A) activity has surged, particularly in copper, where majors like Anglo American remain targets for vertical integration[4]. CEOs are also leveraging partnerships to derisk exploration, such as Anglo American’s collaboration with Finland’s Minerals Group to develop battery value chain opportunities[6]. However, declining ore grades, exploration costs and geopolitical barriers complicate greenfield project development. Rio Tinto’s Nuton leaching technology exemplifies innovation to enhance metal recovery from low-grade ores, achieving 85% recovery rates[2].

1.2 Navigating Geopolitical Fragmentation

The U.S.-China trade war has intensified competition for mineral dominance. China’s export restrictions on gallium and germanium in 2024, coupled with its control over 60% of global lithium refining, underscore vulnerabilities in Western supply chains[9]. In response, CEOs are diversifying sourcing through bilateral agreements, and initiatives such as Australia’s audits of stalled coal and iron ore projects aim to revive $119B in investments[5]. The U.S. Defense Production Act further incentivises alliances with Canadian and Australian firms to build domestic refining capacity[6].

2. Operationalising ESG Commitments

Environmental, social, and governance (ESG) factors now directly influence access to capital and regulatory approvals. Over 75% of institutional investors require ESG compliance for mining investments, prompting CEOs to embed sustainability into core operations[8].

2.1 Decarbonising Operations

Scope 1 and 2 emissions reductions are progressing via renewable energy adoption—BHP’s Pilbara operations now source 50% of power from solar-wind hybrids[7]. However, net-zero targets face capacity hurdles: hydrogen-based steelmaking requires 300MW of electrolyser capacity per tonne, far exceeding global production[2]. Partnerships with equipment manufacturers, like Vale’s Waste to Value program, aim to commercialise low-carbon technologies while achieving circularity outcomes[6].

2.2 Strengthening Community Engagement

Indigenous land rights and benefit-sharing agreements are non-negotiable. Australia’s strengthened Native Title Act mandates equitable profit-sharing, exemplified by Newmont’s drone-based land monitoring systems developed with Aboriginal communities[3][5]. Conversely, protests over cobalt mining in the DRC highlight risks of inadequate governance. Blockchain platforms, piloted by De Beers for diamond tracing, enhance transparency in conflict mineral sourcing[10].

3. Leveraging Digital Transformation

Technological adoption is no longer optional. Deloitte estimates that AI, automation and improved data analytics could boost mining productivity and offset a decade of 28% productivity decline per annum, related to ore quality[8].

3.1 Smart Mining Ecosystems

Industrial IoT and 5G enable real-time asset tracking, while AI optimizes exploration—Freeport-McMoRan’s predictive maintenance systems reduced downtime by 30% in 2024[3]. Control towers, like those deployed by Newmont, integrate drone and sensor data for end-to-end supply chain visibility, mitigating disruptions from geopolitical shocks[3][6].

3.2 Blockchain for Ethical Sourcing

Blockchain’s immutable ledgers address traceability gaps. BHP’s pilot for wellbore rock tracking and Antofagasta’s tire recycling blockchain demonstrate scalability[3][10]. However, the ‘proof-of-work’ protocols that mine the blocks for the chain are extremely energy intensive, which is a sustainability concern, pushing firms toward hybrid models[10]. For example, newer protocols such as ‘proof-of-stake’ can mine blocks using 99% less energy, making the platforms which use that protocol more viable as a solution.

4. Managing Geopolitical and Macroeconomic Volatility

The return of resource nationalism and shifting trade policies demand agile strategies. Over 40% of mining CEOs cite geopolitical instability as their top risk, ahead of commodity price swings[4][9].

4.1 Countering Resource Nationalism

Rising royalties and export bans—such as Indonesia’s nickel ore restrictions—compel localised processing. Joint ventures (JVs) with state-owned entities, like Rio Tinto’s Oyu Tolgoi partnership with Mongolia, mitigate expropriation risks while securing licenses[2][9].

4.2 Hedging Macroeconomic Shocks

Precious metals are regaining prominence as inflation hedges. Gold equities traded at 9x EBITDA in 2024, a 30% discount to S&P 500 averages, attracting contrarian investors[1]. CEOs are rebalancing portfolios toward gold and silver, with Agnico Eagle’s acquisition of Yamana Gold exemplifying consolidation in undervalued sectors[1][4].

5. Optimising Capital and Talent Strategies

Financial discipline and workforce innovation are critical amid capital constraints.

5.1 Capital Allocation and M&A

Active portfolio management is prioritising high-margin assets. Barrick Gold’s divestment of non-core African mines funded expansions in the Americas, while First Quantum’s $1.7B sale of Zambian assets reduced debt[1][4]. Private equity’s $15B deployment into junior miners in 2024 signals confidence in critical minerals[6].

5.2 Upskilling for the Digital Era

Automation requires reskilling 40% of the workforce by 2030. BHP’s AI training programs and partnerships with Australian universities aim to close gaps in data analytics and robotics[5][7]. FIFO (fly-in-fly-out) models continue to evolve with VR-enabled remote operations centers, improving retention in remote regions[5].

6. Building Resilient Supply Chains

CEOs are reengineering supply networks for redundancy and localisation.

6.1 Diversification and Localisation

The EU’s Critical Raw Materials Act mandates 10% domestic extraction by 2030, spurring projects like Sweden’s Kiruna iron ore mine expansion[9]. Tesla’s Warp ERP system, extended to suppliers, enables real-time demand forecasting, reducing lithium procurement lead times by 25%[3].

6.2 Circular Economy Integration

Recycling now contributes to supply shortfalls and decarbonisation efforts, driven by initiatives like Aurubis’ urban mining plants. Rio Tinto’s AP60 smelter recovers 95% of aluminum from scrap, aligning with EU taxonomy requirements[6][8].

Conclusion

The metals and mining industry’s 2025 agenda hinges on strategic agility. CEOs must champion technological disruption while navigating an increasingly fragmented geopolitical landscape. Prioritising critical minerals, ESG compliance, and supply chain resilience will separate leaders from laggards. As Baker Steel notes, mining equities’ deep undervaluation presents a generational opportunity—but only for those who align with the new industrial revolution’s demands[1][6]. Success will require balancing stakeholder capitalism with unrelenting operational excellence, ensuring the sector remains central to global decarbonisation efforts.

Sources [1] Will miners unearth riches for investors in 2025? - Baker Steel Capital [2] Top 10 mining and metals risks in 2025 | EY - Australia [3] Digital technologies for resilient mining supply chains - Infosys [4] Mining & metals 2025: Poised on the chessboard of geopolitics [5] Where Does Australia's Mining Sector Stand in 2025? [6] [PDF] Tracking the trends 2025 | Mining.com [7] 2024 year in review and 2025 outlook: Navigating a complex metals [8] Promoting metals and mining sustainability in critical supply chains [9] Ten global issues to shape mining and metals markets in 2025 [10] Digitalising The Mining & Metals Global Supply Chain - The Assay [11] Future of Mining Australia 2025 [12] Ten global issues to shape mining and metals markets in 2025 [13] Reinvention on the edge of tomorrow - PwC [14] Metals and mining: predictions for 2025 | Wood Mackenzie [15] METS Insight: State of Mining Review into 2025 [16] First Quantum CEO makes Zambia sale a priority for 2025 - Miningmx [17] Five Dynamics That Will Test CEOs in 2025 | BCG [18] 8 Shifts Defining Mining in 2025 – Opportunities & Challenges [19] Gold: Aggressive 2025 Plan and Positive Metallurgy - YouTube [20] Miners flag pursuing inorganic growth in 2025 - Mining.com.au [21] What's important to the CEO in 2025 - PwC [22] Top 10 mining and metals risks in 2025 | EY - Global [23] Digital Transformation in Steel Manufacturing: Optimizing Supply [24] The role of digital twins and AI in enhancing decision-making ... - BHP [25] Top 6 Trends Making Mining More Sustainable in 2025 [26] Supply Chain Trends for 2025: Innovation, Sustainability